International Economists Pressure RBNZ: Further OCR Cuts Expected as Economic Recovery Stalls

AUCKLAND, NEW ZEALAND — December 2, 2025 — Despite the Reserve Bank of New Zealand (RBNZ) signalling a potential pause in its aggressive easing cycle, a prominent collection of international and domestic economists maintain that the central bank will be forced to implement further cuts to the Official Cash Rate (OCR) in early 2026. This prediction comes as economic activity remains weaker than anticipated, with significant spare capacity still present in the New Zealand economy.

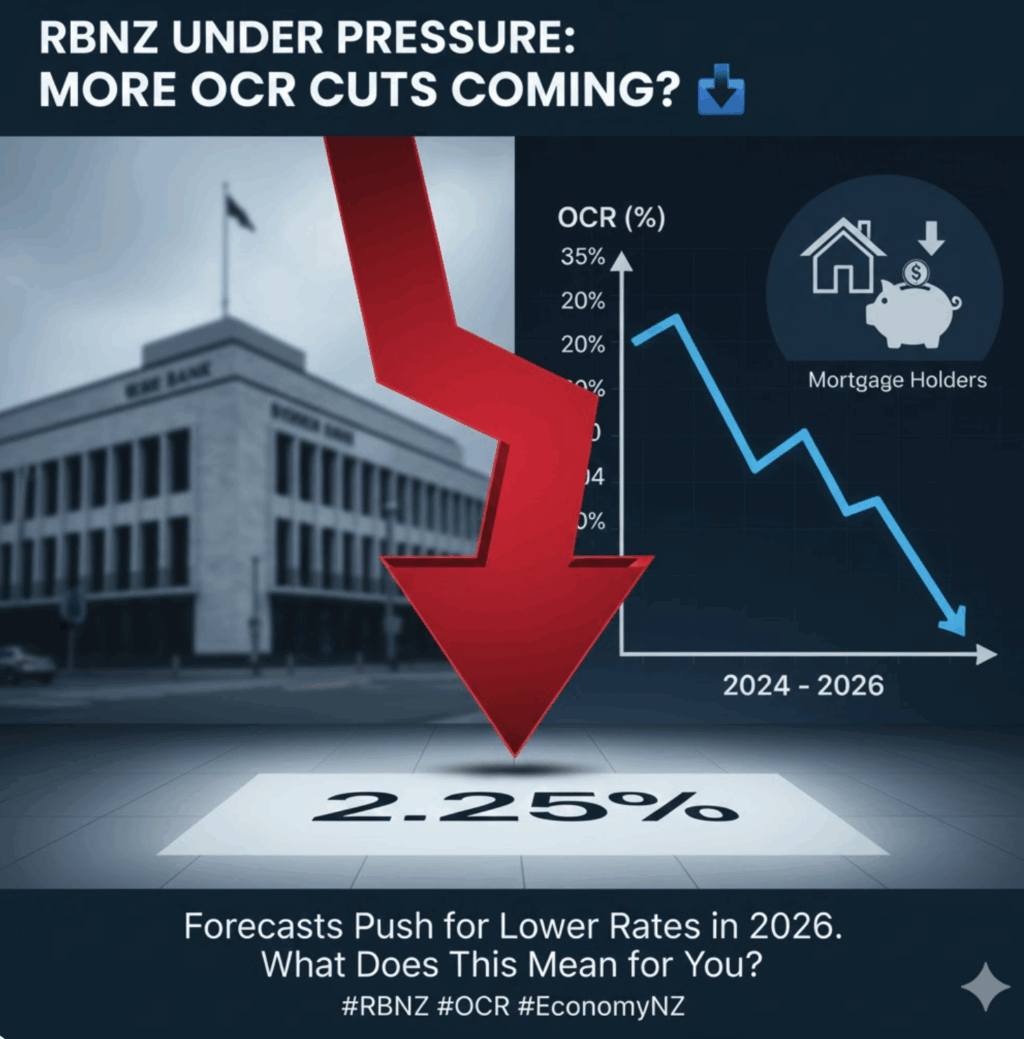

The RBNZ’s Monetary Policy Committee (MPC) recently lowered the OCR to 2.25% at its November 2025 meeting—a sharp reduction from its August 2024 peak of 5.5%. While the RBNZ’s own forecasts now show the OCR stabilising at or near this level, with a minor low of 2.20% projected, the market consensus among leading international economic desks is leaning towards a need for greater monetary stimulus.

🛑 The Case for More Easing

Economists argue that several factors make further OCR cuts unavoidable if the RBNZ is to meet its mandate of supporting maximum sustainable employment and getting inflation back to the 2% midpoint of its target range.

- Sluggish Economic Recovery: The New Zealand economy has struggled to gain traction, with GDP contraction in the middle of 2025 being more severe than expected. While forward-looking indicators are showing modest improvement in areas like exports, sectors reliant on domestic demand, such as retail and construction, remain weak.

- High Spare Capacity: Data indicates that there is still significant spare capacity in the domestic economy, particularly reflected in a softening labour market with an unemployment rate that has climbed. This “slack” is the main factor economists believe will keep downward pressure on inflation, providing the RBNZ with the justification to ease further.

- Need to Boost Confidence: Lowering the OCR further provides a clear signal to both households and businesses that the RBNZ is committed to supporting the recovery. According to some analysis, confidence remains brittle, and a bolder cut could mitigate the risk that the economy recovers more slowly than necessary.

⚖️ RBNZ’s Cautious Stance

The RBNZ, however, is proceeding with caution. The MPC’s November statement suggested a “neutral bias,” indicating the high hurdle for any future easing.

- Inflation at Target Edge: Annual CPI inflation remains at the top of the RBNZ’s 1-3% target band. While the Bank expects inflation to return to the 2% midpoint by mid-2026, it is wary of any upside risks that could be triggered by overly aggressive rate cuts, such as a strong, unexpected rebound in housing demand or commodity prices.

- Lagged Effects of Previous Cuts: The RBNZ is keen to wait for the full effect of the substantial rate cuts already delivered over 2024 and 2025 to flow through the economy, particularly as a large number of mortgage holders are still rolling off higher fixed rates.

🔮 What It Means for New Zealanders

If the international economists’ predictions prove correct, further OCR cuts in the new year would bring welcome news to mortgage holders who would see a faster reduction in their borrowing costs. Conversely, savers relying on term deposits would face even lower returns. The pressure now mounts on the RBNZ as it heads into 2026, with its next review scheduled for February 18th, to balance the need to stimulate a sluggish economy against the risk of reigniting inflationary pressures.

The consensus appears to be that the RBNZ’s current forecast of 2.25% being the bottom may be tested if economic data fails to show a convincing recovery in the coming months.