The Year of the Refix: Why New Zealand Home Loan Costs Are Still Set to Fall

By Lions Roar Aotearoa Economic Desk

AUCKLAND, NEW ZEALAND (Monday, February 2, 2026) — In a curious twist of financial timing, New Zealanders are being told that while overall interest rates may have bottomed out and started to climb, the actual amount households pay for their mortgages will likely continue to drop through the first half of 2026.

According to BNZ Chief Economist Mike Jones, the country is currently navigating the “tail end” of a massive repricing event. Speaking to RNZ’s Susan Edmunds, Jones noted that while 2025 was the official “Year of the Refix”—with a record 81% of fixed-rate borrowers renewing their loans—the momentum is far from over.

📊 The 2026 Refixing Pipeline

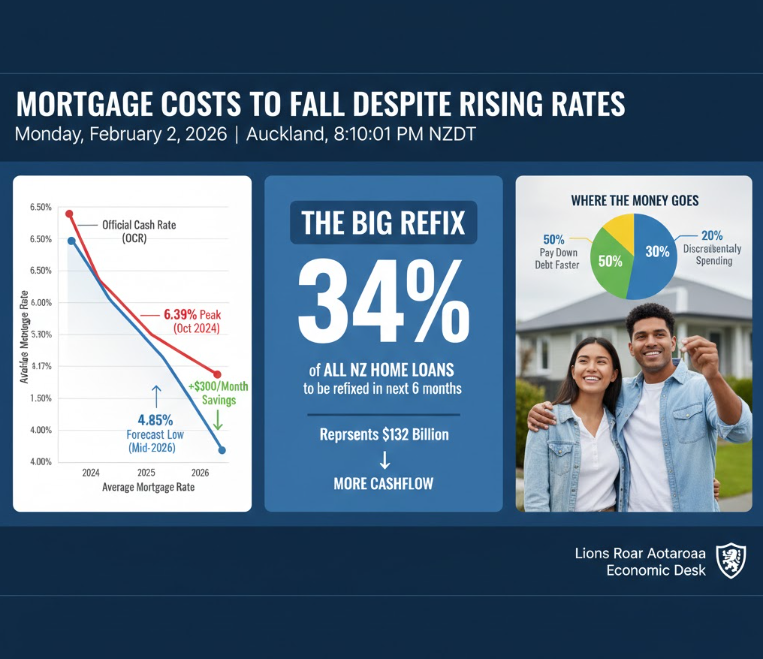

This year, approximately 68% of all fixed-rate loans are due for renewal. The concentration of these expiries is particularly high in the next six months, representing a staggering $132 billion (or 34% of total borrowings).

- Average Rate Paid (Nov 2025): 5.17%

- Peak Rate (Oct 2024): 6.39%

- Forecast Low (Mid-2026): ~4.85%

The lag between official rate changes and household reality means that even as banks start nudging their advertised rates higher, many homeowners are coming off loans fixed at much higher levels (e.g., 5.74%) and refixing at lower current market rates (e.g., ~4.5%).

🏠 Where Is the “Refix Windfall” Going?

The “easing pipeline”—which Jones estimates still has about 25 basis points worth of relief to deliver—is creating a significant cash flow injection for many families. However, this extra money isn’t necessarily fueling a massive shopping spree.

- Debt Reduction: Many Kiwis are choosing to keep their repayments at the same level, effectively paying off their principal faster.

- Cost of Living Buffer: For others, the savings are being immediately swallowed by higher insurance, rates, and grocery costs.

- Cautious Discretionary Spending: While some money is returning to the retail sector, the recovery remains “patchy,” as households remain fatigued by three years of economic instability.

🧭 Expert Strategy: “Don’t Miss the Boat”

With markets increasingly pricing in an earlier-than-expected hike to the Official Cash Rate (OCR)—potentially as early as late 2026 due to sticky inflation—forecasters are warning that the window for low long-term fixes may be closing.

“We suspect we’re in for a period of consolidation,” Jones warned. While the average rate paid will keep falling until mid-year, the “menu of options” for those refixing today is starting to look slightly more expensive for longer terms.