KiwiSaver Crisis: Soaring Hardship Withdrawals Fuel Fears of a ‘Lost Generation’ of Retirees

AUCKLAND, NZ — A dramatic and sustained surge in KiwiSaver hardship withdrawals is exposing a deep and widening fissure in New Zealand’s financial landscape, as a growing number of citizens are forced to raid their retirement funds merely to survive the mounting cost-of-living crisis.

The situation, marked by emotional testimony from those grappling with destitution and a sharp spike in official withdrawal figures, has prompted experts and financial mentors to raise the alarm, warning that the country is on the verge of creating a ‘lost generation’ who will reach retirement with minimal or zero savings.

The Desperation on the Front Lines

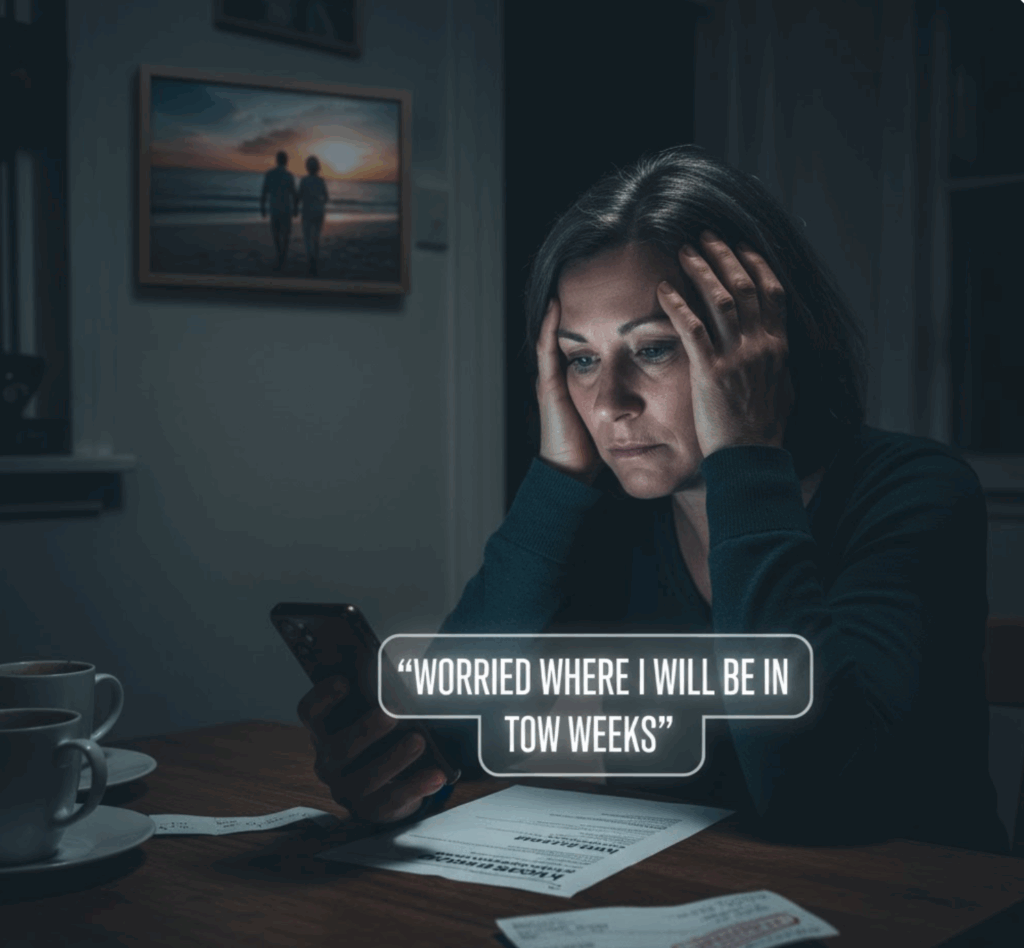

The crisis is perhaps best encapsulated in the words of one KiwiSaver member, identified only as Sarah (not her real name), who recently completed the arduous process of applying for a hardship withdrawal. Her statement, “Worried where I will be in two weeks,” has become a stark, painful mantra for thousands of New Zealanders facing similar desperate choices.

In an interview, Sarah described the invasive and stressful process required to access her own money—a process deliberately stringent to protect retirement funds, but which, for those in genuine crisis, feels like an added punishment.

“My choice is no longer ‘comfortable retirement vs. poor retirement’—it is ‘keep my home vs. lose everything’,” she stated, challenging the notion that these withdrawals are being made frivolously. She highlighted the strict eligibility criteria: applicants must be effectively destitute, often having less than $\$3,000$ cash to their name, and must subject their entire financial life, including a partner’s details, to intense scrutiny.

“The process is invasive and onerous. You cannot apply until you are effectively destitute,” she added. “There is no guarantee that the hardship withdrawal will be approved, so as you watch your savings dry up, your stress levels ramp up, your mental health suffers and dark thoughts often crowd your mind. Sleep is non-existe1nt.”

📈 Record-Breaking Figures: A $49 Million Band-Aid

The anecdotal evidence is supported by cold, hard statistics. Data released by Inland Revenue (IRD) confirms a record-breaking surge in withdrawals for the purpose of financial hardship:

- In October 2025 alone, a staggering $49.4 million was withdrawn from KiwiSaver funds due to hardship. This is a significant increase from $\$38.4$ million withdrawn in October 2024.

- The total number of members making hardship withdrawals in October 2025 reached 5,520, up substantially from 4,490 a year prior.

- For the 2024-2025 financial year, 45,870 members accessed their retirement savings for financial hardship, a chilling jump from the 8,250 members who did so in the 2015 financial year.

KiwiSaver providers themselves have expressed concern, with some suggesting that the hardship withdrawal mechanism—intended as an absolute last resort—is now being viewed and used as a de facto emergency fund.

One provider noted that the average hardship withdrawal is approximately $\$8,800$, an amount that, while crucial for immediate relief, could reduce a person’s final, inflation-adjusted retirement balance by as much as $\$40,000$ to $\$50,000$ due to lost compounded returns.

🛑 The ‘Leaky Tap’ and Calls for Systemic Change

The Retirement Commissioner, Jane Wrightson, has publicly highlighted the sharp increase in hardship withdrawals in her recent three-yearly review of retirement income policy, describing the trend as a serious threat to the scheme’s long-term integrity.

Financial mentors, who often guide applicants through the gruelling process, are equally concerned. They stress that the withdrawals are, at best, a temporary solution to deep-seated issues.

“From my perspective, a KiwiSaver hardship withdrawal is no more than a 13-week band-aid,” stated one financial mentor. “In this period, we need to find more permanent solutions to what are very fundamental underlying issues—too little income, too much debt, too many expenses.”

The issue of “manipulation” has also been raised by providers. While acknowledging that most applicants are genuinely desperate, some industry figures suggest that applicants have learned to let payments (like rent or mortgage) fall into arrears specifically to meet the strict legal criteria for a withdrawal. This, they argue, shows the pressure on families is now so severe that they are intentionally worsening their credit positions just to unlock their own money.

However, financial mentors, including those represented by bodies like FinCap, strongly oppose any tightening of the criteria. They argue that any move to restrict access would only hurt the most vulnerable.

“Our clients are generally in financial crisis,” stated one representative. “Budgets will be in deficit, and many will have debts and obligations that are in arrears. The ongoing cost-of-living increases, without commensurate increases in incomes, have seen the applications ramp up.”

🌍 Cultural and Community Impact

The crisis is not evenly spread. Financial advisors have noted the disproportionate impact on certain communities, particularly Pacific families. Cultural traditions often place significant financial obligations on individuals to support extended family members, church communities, and villages back in the islands. When a crisis hits, and a family lacks emergency savings, KiwiSaver becomes the only remaining option, exacerbating a cycle of debt and impacting long-term goals like home ownership.

“They’re already in a position where they don’t know what else to do,” noted a community advisor who works with Pacific families.

🔑 Last Resort: What Can Be Done?

The consensus among financial literacy groups, including Sorted, the government-backed service, is clear: KiwiSaver withdrawal must be the absolute last resort. They urge individuals facing hardship to explore all other avenues first:

- Seek Financial Mentoring: Free, confidential advice is available through services like MoneyTalks.

- Contact Lenders: Banks and financial institutions are legally required to discuss options for restructuring loans or providing short-term relief during unforeseen hardship.

- Government Support: Explore all available support from Work and Income (WINZ), including accommodation supplements and help with urgent costs, which often must be exhausted before a KiwiSaver hardship application is even considered.

- Temporary Suspension: Suspending KiwiSaver contributions for up to a year is an option that provides short-term cash flow without raiding the existing balance, allowing it to continue growing.

Ultimately, the soaring numbers underscore a profound societal problem: for a significant portion of the population, the cost of living has outstripped income and basic emergency savings. Until systemic changes address the underlying issues of low wages and high expenses, KiwiSaver will continue to act as an involuntary sacrifice, protecting people from immediate destitution at the heavy, long-term cost of their financial security in retirement.